Last Tuesday, October 8, 2016, England enacted the second phase of its Help to Buy plan, which encourages low-deposit borrowing for purchases of newly built and already existing homes. The first phase of the plan was enacted this April, and the plan is set to run for the next three years.

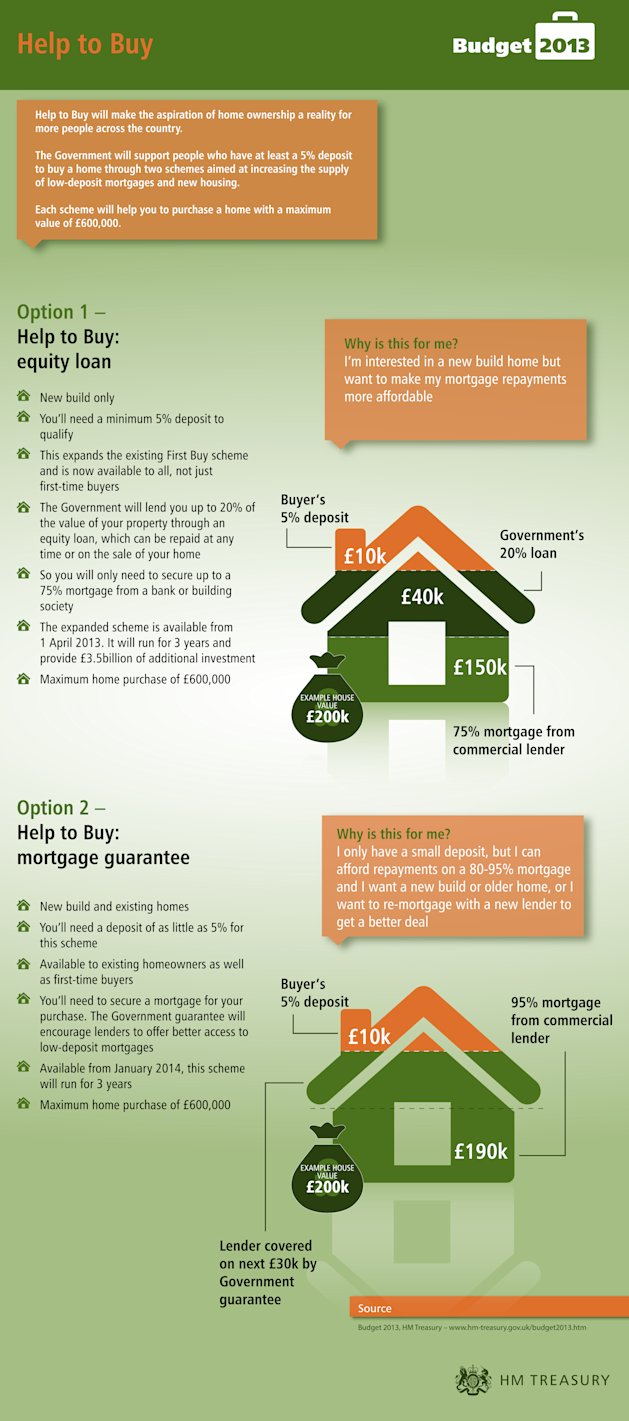

Under the first phase, the government will provide a 20% equity loan toward the purchase of a new home priced at £600,000 or less when the purchaser deposits 5% of the purchase price up front. These loans are interest free for the first five years, accrue at an interest rate of 1.75% for the sixth year, and accrue at a floating rate of 1% plus the Retail Price Index inflation rate for every subsequent year.

{kind=link}

Under the second phase, registered lenders, who have paid the necessary fees to the government, may offer a mortgage covering up to 95% of the purchase price of a new or existing home valued at £600,000. The purchaser, however, is required to deposit 5% of the value up front. In return, lenders will receive a seven-year guarantee from the government covering 15% of the loan value.

The four participating lenders have already revealed their rates, but some lenders have been more reluctant to join the program. RBS and NatWest are offering a two-year, no fee fixed-rate mortgage (FRM) starting at 4.99% for those depositing 5% of the home value. Halifax is offering a starting rate of 5.19% with a £995 fee. While somewhat competitive for the low-deposit market, these rates are not competitive with higher-deposit rates.

Chancellor George Osborne hopes to encourage lending to a more risky sector of borrowers. Proponents of the plan, like Stephen Noakes, mortgage director at Lloyds Banking Group, said the proposals will help first-time and low-income buyers by providing “a genuine solution to the challenge of raising a deposit.”

Critics question the plan’s effectiveness in benefiting low-income, first-time buyers. “The main beneficiaries will be the banks, estate agents, and people who own houses already – who tend to be older and richer,” says Jonathan Portes, Director of the National Institute of Economic and Social Research.

Many, including members of Parliament, worry that this plan is akin to government-sponsored enterprises (GSEs) like Fannie Mae in the United States and could contribute to a speculative housing bubble (for a comprehensive analysis of how GSEs contributed to the subprime mortgage crisis in 2008 by reducing standards of mortgage-back securities (MBSs), read this paper). Housing prices in England are already expensive, and rising prices would make homes unaffordable for the majority of people. Moreover, the second phase of the Help to Buy plan delegates screening responsibilities to the banks, which were partly responsible for the financial instability caused by sub-prime mortgage lending in England.

Addressing these concerns, Osborne subsequently assigned the Bank of England‘s Financial Policy Committee the power to review the plan annually instead of three years as originally intended. The Bank of England would be able to make recommendations to the Treasury to lower the cap and impose higher fees on loans. The next three years will be telling.