The banking industry, served with a cocktail of financial re-regulation and an anticipated interest rate increase, may be in for a headache.

The banking industry has gradually been adapting itself to the regulation regime introduced by Basel III, introduced after the 2008 Financial Crisis to account for its deficiency in focusing only on capital requirements. The older Basel II regime has been reformed to increase not only the levels of certain “tiers” of capital in capital requirements, but also to encapsulate two additional areas for regulation: liquidity and leverage. Leverage regulations are further set to change. Questions, however, arise as to whether liquidity regulation in this environment is the best time for financial re-regulation.

One of the new innovations of Basel III’s liquidity aspect is the “Liquidity Coverage Ratio” (LCR). In broad strokes, LCR is meant to bolster the banking industry’s resiliency to liquidity shocks. To do so, the LCR is meant to ensure that banks continually hold a certain minimum level of liquidity assets to survive a “stress scenario” for thirty days. The specifics of what constitutes the stress scenario, the haircuts for different assets, and other regulatory mechanisms have been implemented domestically by the Federal Reserve, the OCC, and the FDIC.

One of the new distinctions of Basel III regulation: all cash is no longer equal. Liquidity regulation has conceptually distinguished between deposits held by banks. “Operational deposits,” cash held by the bank that is “necessary” to provide operational support for an investor’s bank-operated services, faces more lenient haircuts than “non-operational deposits,” which is “everything else.”

Basel III’s distinction of deposits highlights the theory of the “stickiness” of cash: operational deposits should remain relatively stable, even in times of stress, as investors continue to use bank-services; non-operational deposits, however, are untied to any need with the bank, and are thus “hot money”—here one moment, gone the next. In a stressed environment, hot money runs to safer havens; in non-stressed environments, it runs to higher yields. The LCR is meant to ensure that banks are more adequately protected by requiring higher levels of high-quality liquid assets (HQLA) against non-operational deposits and continually monitoring a bank’s LCR to ensure it does not go below 100%. Certainly more stable, but as JPMorgan has noted, “those benefits come at a price, notably limited and potentially negative returns. When compared to the return potential for operating deposits used to fund loans, the return on non-operating deposits deployed against HQLA is significantly less, limiting return potential for both the bank and the company.”

Lower profitability for both banks and investors has meant a challenge in the current low-interest rate environment. The Wall Street Journal has recently reported on the issue. In a more normal environment, the implementation of LCR should drive deposits away from banks as they become unprofitable by the banks to hold them. In turn, investors seek to find higher yields for their cash elsewhere, perhaps reducing their liquidity by selling cash for financial instruments. But with concerns about volatility in the markets, an anticipated interest-rate increase, and 3-month treasury bills recently hitting a 0% yield, where’s the money to go? Institutional investors, as the WSJ has noted, have faced a quagmire: discouraged from increasing their non-operational deposits, being charged for their currently existing ones, facing low yields, and anticipating volatility, their cash stockpiles can either be converted into less liquid instruments or face negative-yield deposit rates.

However, the problem may not fall to just institutional investors. LCR has presented problems for banks in attempting to determine just how much operational as opposed to non-operational deposits they hold. An August Credit Suisse analyst report has touched on the issue. With an anticipated increase in interest rates to follow this year, Pozsar & Sweeney have attempted to analyze how the anticipated “lift-off” in interest rates will affect the short-term health of bank. One particular area of difficulty they note is the flight of non-operational deposits to higher yields: hot money is already facing negative yields, institutional investors anticipate an even more negative rate, and at the first sight of safer havens, they will run away. But how quickly will this occur and just how much “hot money” does every bank have? Pozsar & Sweeney note a discrepancy in the confidence of earnings calls as opposed to back-office modelers.

As the exact amount of non-operational deposits is hard to determine, banks will have to model their estimates of what they hold. Due to the relatively new conceptualization of non-operational deposits, Pozsar and Sweeney note, the “potential for model risk abounds.” Here is what they have to say:

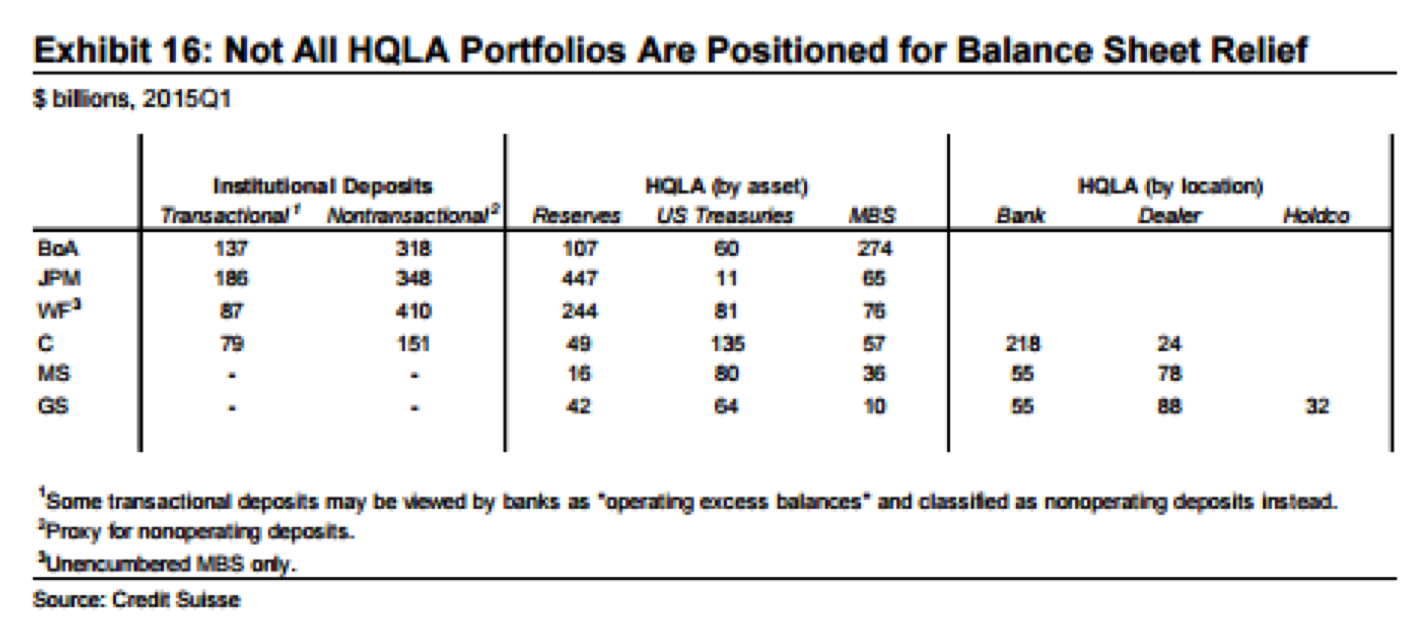

“Of particular interest is how much of non-operating deposits are those of financial institutions (such as asset managers, hedge funds, private equity funds and FX reserve managers) with a 100% HQLA requirement. Only one of the top four U.S. banks has disclosed that of the $390 billion of deposits it had from financial institutions as of the first quarter of 2015, $200 billion is non-operating (with a 100% HQLA requirement). Assuming a similar split at the other three top U.S. banks points to at least an additional $450 billion of such deposits in the system. According to the U.S. Flow of Funds accounts, financial institutions hold $1.1 trillion in deposits. If we are right, 60% of these are non-operating.

Losing these deposits will be a non-event for banks that have more reserves than non-operating deposits. As deposits leave for money funds, banks give up reserves, which the Fed will swap into RRPs and give to money funds. The only trade that occurs in the financial system is the Fed swapping reserves for RRPs – a non-event in markets.

As deposits leave, these banks will gain balance sheet relief and remain LCR compliant, freeing them up to do whatever they please with their surplus capital: buy back debt, buy back stock or compete retail deposits away from others – all positives for their equity price.

Life may not be so simple for banks that have fewer reserves than non-operating deposits, however. If deposits leave faster or in greater volume than assumed, these banks will have to choose between one of three options: (!) paying up for wholesale deposits in order to slow their outflow to a pace more in line with their HQLA profile (a first resort response); (2) repoing U.S. Treasuries from their HQLA portfolio to raise the liquidity to finance deposit outflows (as a next resort); or (3) sell U.S. Treasuries and other HQLA assets such as agency MBS right in the middle of a hiking cycle (as a last resort option).

Whichever one of these scenarios will dominate, one thing is for sure. These banks either won’t gain balance sheet capacity as fast as those that are “over-reserved.” Or if they do, the higher funding costs and trading losses incurred will weaken their ability to compete for (or much worse, retain) retail deposits – all potential negatives for their equity price.

A rising tide – rising interest rates – may not lift all boats as is typically the case during hiking cycles. The implication for bank equities is straightforward (see Exhibits 16).”

Source: Poszar & Sweeney, “A Turbulent Exit,” Credit Suisse Economic Research, 28 Aug. 2015, p. 17

The future will either come to validate Poszar & Sweeney’s analysis or not. However, one thing is certain: the problem is real. Having to face both financial re-regulation and an anticipated interest-rate increase, banks and institutional investors have a potentially potent cocktail in their hands.

All Cash Is Not Created Equal- Basel III’s Liquidity Coverage Ratio & its Effects (PDF)