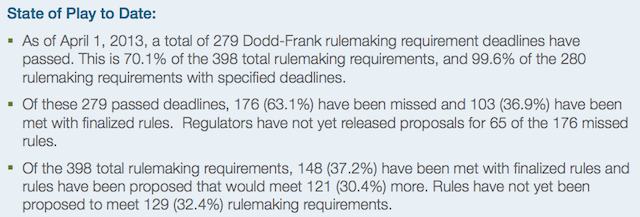

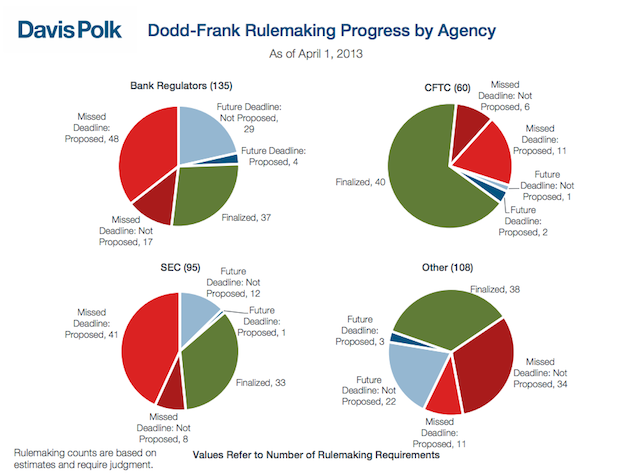

[Editor’s note: The following post is from Davis Polk’s April 2013 Dodd-Frank Progress Report, generated using the Davis Polk Regulatory Tracker.]

[Editor’s note: The following post is from Davis Polk’s April 2013 Dodd-Frank Progress Report, generated using the Davis Polk Regulatory Tracker.]

The Consumer Financial Protection Bureau has announced a new rule (the “Ability-to-Repay rule”) requiring mortgage lenders to ensure that potential borrowers will be able to repay their mortgages. The CFPB is charged with amending Regulation Z, which carries out the Truth in Lending Act. The CFPB also implements the ability-to-repay requirements under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”). Under Dodd-Frank, creditors must make a reasonable and good faith determination that borrowers have a reasonable ability to repay the loan.

The Ability-to-Repay rule is aimed at protecting American consumers. According to the CFPB Director, the “Ability-to-Repay rule protects borrowers from the kinds of risky lending practices that resulted in so many families losing their homes.”

Under the new rule:

In assessing whether a borrower will be able to repay their loan, lenders must generally consider the following underwriting factors: 1) current or reasonable expected income or assets, 2) current employment status, 3) the monthly payment, 4) monthly payment on any simultaneous loan, 5) the monthly payment for mortgage-related obligations, 6) current debt obligations, 7) monthly debt-to-income ratio, and 8 ) credit history.

While much attention has been paid to increasing taxes on high-income earners as a result of the fiscal cliff compromise (the American Taxpayer Relief Act of 2012), less attention has been paid to the compromise’s corporate tax provisions. In a recent Tax Department Update, Latham & Watkins summarizes the effects of the compromise on both individuals and businesses. The Update also covers the compromise’s effects for various energy-related credits, including the extension of a tax credit for qualified wind facilities. The Update is available for download here.

As part of the Dodd-Frank Act’s requirement for regulated and centralized derivatives trading, many nonfinancial companies that use derivatives may be required to register with the CFTC. However, there is an exception for a “nonfinancial end user.” In general, to qualify as a non-financial end user, the company must not be a swap dealer, major swap participant or other “financial entity.” Additionally, the derivatives must be used as for commercial, rather than investment, purposes. WilmerHale’s recent Corporate and Futures and Derivatives Alert provides a thorough explanation of the application of this exception for nonfinancial companies.

Gibson Dunn recently hosted its ninth-annual webcast, “Challenges in Compliance and Corporate Governance.” Corporate Counsel viewed the webcast and derived seven takeaways for 2013. Among these lessons is that firms should broaden their focus. Between the SEC’s regulations on conflict minerals and sanctions on Iran, broad-based compliance efforts are necessary. Another lesson is that firms should not forget the compliance tone in the middle. While many compliance officers focus on setting the tone for upper management, it is often middle managers who receive tips and should be trained on proper compliance procedures. Check out the other takeaways here.

Late last year, the Federal Reserve issued guidance on its new framework for supervising large financial institutions. The Federal Reserve’s primary objectives will be to increase the resiliency of financial institutions, and to reduce the impact of an institution’s failure on the broader economy. Changes include a greater emphasis on recovery and orderly resolution planning as required by Dodd-Frank. In a recent publication, Sullivan & Cromwell reviews the specifics of the recent changes and explains how their implementation may differ from the previous regulatory framework.

The expectation that courts will recognize and enforce the insolvency proceedings of foreign courts is essential to certainty and predictability of cross-border transactions. This is especially important where the two nations’ bankruptcy laws materially differ. Three recent decisions in the U.S. and U.K. call into question whether such an expectation is reasonable. In one of the cases, the Fifth Circuit held unenforceable a $3.4 billion restructuring plan approved by a Mexican court as “manifestly contrary to the public policy of the United States.” The Fifth Circuit took issue with the Mexican court’s decision that shareholders receive $500 million in value while higher-ranking creditors receive only 40 percent of their claims. In a recent client alert, DLA Piper explains the implications of these decisions for certainty and predictability of cross-border transactions.

The U.S. District Court for the District of Columbia recently dismissed a lawsuit challenging recent amendments to CFTC Rule 4.5. With limited exceptions, the amendments require registration by investment companies that trade in futures, options, and commodities. The plaintiffs, the Investment Company Institute and the U.S. Chamber of Commerce, argued the amendments were arbitrary and capricious in violation of the Administrative Procedure Act and that the CFTC failed to perform adequate cost-benefit analysis. In rejecting these arguments, the court found that the link between unregulated derivatives and the financial crisis provided an adequate basis for the amendments. In a recent Client Alert, Ropes & Gray explains the court’s reasoning and the decision’s implications for registered investment companies.

In a recent Client Alert, Wilson Sonsini reviews the 2012 proxy season, finding it “evolutionary, rather than revolutionary.” In the second year of the say-on-pay requirement, shareholder support for executive compensation averaged about 90 percent. Only three percent of say-on-pay proposals failed to garner the necessary majority of shareholder votes. Moreover, proxy access shareholder proposals—proposals by large shareholders to include their director nominees in the company’s proxy statement—enjoyed modest success in 2012. The Alert provides in-depth analysis of these results and recommendations for 2013.

A jury in Los Angeles recently found three former officers of the failed IndyMac Bank liable for $168 million in losses. The suit, brought by the FDIC, sought damages resulting from construction loan losses by the bank’s Homebuilder Division. In a recent Client Alert, Manatt analyzes the result and provides “lessons learned” from the jurors’ quick decision. Among other lessons, the firm suggests that officers are likely to be held to a higher standard than are directors when they actually approve the loans, especially in California where courts have consistently refused to extend the business judgment rule beyond directors.

The CFTC recently published a series of no-action letters, providing for: 1) a limited exemption for swap dealers from the prohibition against association with certain persons subject to statutory disqualification, 2) an exemption for swap dealers from the requirement to disclose counterparties when the entity has a reasonable belief that the disclosure would violate foreign laws, and 3) a limited exemption for certain futures commission merchants from the requirement that the chief compliance officer certify the annual report. In a recent Financial Alert, Goodwin Proctors has a full summary of these no-action relief letters, as well as an update on other regulatory news.

The Securities and Exchange Commission recently adopted a new, stricter rule governing risk management and operation standards for registered clearing activities. This new Rule, 17 Ad-22, will become effective 60 days after its publication in the Federal Register.

The Rule requires registered clearing agencies that perform central counterparty services to establish, maintain and enforce written policies and procedures reasonably designed to limit their exposure. At minimum, they must measure their credit exposure at least once per day and maintain margin requirements to limit their credit exposure to participants, using risk-based models and parameters. The procedures must be reviewed monthly, and the models must be validated annually.

The Rule is an attempt “to ensure that clearing agencies will be able to fulfill their responsibilities in the multi-trillion dollar derivatives market and more traditional securities market.” It is part of an effort to promote financial stability by improving accountability and transparency in the financial system. It was adopted in accordance with the Dodd-Frank Act, which gave the SEC greater authority to establish standards for clearinghouses.

In general, clearing agencies act as middlemen to the parties in a securities transaction. They play a crucial role in the securities markets by ensuring the successful completion of operations and avoiding the risk of a defaulting operator. In addition, they ensure transactions are settled on time and on the agreed-upon terms.

The rule is similar to the Supervisory Capital Assessment Program, publicly described as the bank “stress tests.” This examination, conducted by the Federal Reserve System, measured the financial strength of the nation’s 19 largest financial institutions. The stress tests measured whether banks had enough capital to weather a downturn with enough funds to continue lending. Like the new Rule, the stress tests were intended to reduce uncertainty surrounding the financial system, while building up transparency and investor confidence.

Under the new Rule, clearing agencies will have to maintain sufficient financial resources to withstand, at a minimum, a default by the participant group to which it has the largest exposure in extreme (but plausible) market conditions. In addition, the clearing agencies will now be required to calculate and maintain a record of the financial resources that would be needed in the event of a participant default. Clearing agencies must perform the calculation quarterly, or at any time upon the SEC’s request, and must post on their websites annual audited financial statements within 60 days of fiscal year-end.

The Rule also requires clearing agencies to implement membership standards for central counterparties reasonably designed to: 1) provide membership opportunities to persons who are not dealers or security-based swap dealers, 2) not require minimum portfolio size or transaction volume. Those who have a $50 million portfolio should also be able to obtain membership, provided they comply with other reasonable membership standards.

Federal Reserve Governor, Daniel Tarullo, recently discussed an upcoming proposal to alter the regulation of foreign banks in the U.S. The proposal would require large foreign banks to establish “a separately capitalized top-tier U.S. intermediate holding company.” The holding company would be “required independently to meet all U.S. capital and liquidity requirements as well as other enhanced prudential standards required by the Dodd-Frank Act.” In a recent Client Memorandum, Davis Polk suggests that the proposal “could have profound negative consequences” for both foreign banks in the U.S. and U.S. banks abroad by adding “fuel to the growing trend toward regionalization of global banking.” The proposal is still under consideration and more details are anticipated “in the coming weeks.”

The Dodd-Frank Act amended the Commodities Exchange Act to require clearing of certain swaps through a derivatives clearing organization. This includes fixed-to-floating swaps, basis swaps, forward rate agreements, and overnight index swaps. The CFTC recently issued final rules to implement this requirement and issued two no-action letters “that provide time-limited relief from the clearing requirement for certain swaps.” In a recent Legal Alert, Bingham McCutchen details the requirements, the timing of their implementation, and safe harbors provided by the no-action letters.

In a recent Corporate Finance Alert, Skadden provides guidance on how to avoid prohibited communications when contemplating a securities offering. Section 5 of the Securities Act prohibits “activities intended to stimulate interest in a securities offering prior to the filing of registration statement.” Violations of this prohibition are commonly referred to as “gun jumping.” The Alert outlines the types and timing of permitted and prohibited communications, as well as suggestions for a company policy on relevant social media communications.

The Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”) has changed the landscape of executive compensation in the United States in favor of greater disclosure. Dodd-Frank requires publicly traded companies to disclose “information that shows the relationship between executive compensation actually paid and the financial performance of the [company].” 15 U.S.C. § 78n(i). Investors can discern what was actually paid to executives and the financial performance of the company in the proxy statement by looking to their company’s “Compensation Discussion and Analysis” and “Summary Compensation Table.”

The requirement for disclosure of pay and performance, coupled with the new ability for shareholders to have a “say on pay” has resulted in increased scrutiny from shareholders. The new “say on pay” regime has allowed shareholders to have a non-binding vote on executive compensation. Even though this vote is non-binding, Boards of Directors are paying attention to potential negative feedback from shareholders.

Because of “say on pay” voting, proxy advisory firms such as Glass Lewis and Institutional Shareholder Services have become more relevant. These firms advise investors whether to vote yes or no on a company’s executive compensation provisions. Because of this new scrutiny, companies are more likely to take actions to ensure they receive a recommended vote of “yes” from these proxy advisory firms. If executive compensation payments appear excessive, the likelihood of a shareholders being advised to vote against executive compensation plans increases.

Therefore, many companies have begun to precede the Summary Compensation table in the proxy report with a “Realized Pay” or “Realized Compensation” table. This additional disclosure reveals the compensation actually realized in the years shown by the named executives according to their W-2 forms. The rationale often given for the additional disclosure is that the numbers in the Summary Compensation table do not show exact figures, but instead show figures for the “fair value” of shares/options awarded. These fair values are based on accounting principles and models that estimate the potential worth of awards, instead of exact earned amounts. For example, the most recent proxy statement for Hewlett-Packard Company states that in 2011, Catherine Lesjak, R. Todd Bradley, and Vyomesh Joshi realized $2.8 million, $3.0 million, and $2.7 million, respectively. The Summary Compensation table states their 2011 compensation as $11.0 million, $10.7 million, and $9.8 million. These numbers are strikingly different. The realized pay table and the summary compensation table present different data; they are not perfect substitutes for one another. The Realized Pay table shows the money the executive took home in a given year. The Summary Compensation Table shows the salary, bonus, and the equity awards the company granted in a given year (not the equity awards that vested or were cashed-in in a given year).

We are still waiting for guidance from the Securities Exchange Commission on the definition of executive compensation “actually paid.” In the meantime, it is reasonable to expect companies to continue to move in the direction of disclosing realized pay.

On November 8th, U.S. exchange operator CME Group filed a lawsuit against the Commodities Futures Trading Commission (CFTC) in the United States District Court for the District of Columbia, asking for an injunction to prevent the CFTC from requiring CME Group to report private data to a third party. In the lawsuit, CME Group alleged that the regulator overstepped its authority under the Dodd-Frank Act by requiring CME Group to report non-public swaps transactions data to CFTC-certified Swap Data Repositories (SDRs), which is in turn released to federal regulators to be used to monitor the market. (more…)

In August 2012, six federal financial regulatory agencies issued a proposed rule to implement Section 1471 of the Dodd-Frank Act which sets forth appraisal requirements for “higher-risk” mortgage loans.

The intended purpose of the proposed rule is to tighten valuation standards for homes in order to reduce the risk of appraisal fraud, a move meant to reassure creditors, borrowers, and investors alike. Section 1471 was created as part of Congress’ intention to prevent the use of false or inflated appraisals in obtaining mortgages. If the proposed rule is finalized without amendment, lenders seeking to issue high-risk mortgage loans will be “unable to value properties on the basis of broker-price opinions, automated valuations, or drive-by appraisals”. The proposed rule would affect mortgages with annual percentage rates (APRs) at designated levels above the Average Prime Offering Rate (APOR). First-lien loans (such as standard mortgages) with an APR 1.5 percentage points above the APOR would be classified as a higher risk mortgage under the proposed rule, while first-lien jumbo loans with APRs 2.5 percentage points above, and subordinate-lien loans with an APR 3.5 percentage points above the APOR would similarly be considered higher-risk.