On November 20, 2013, in a broadcast streamed live on the internet, the CFPB unveiled the long awaited final rule that contains the Integrated Mortgage Disclosures under the Real Estate Settlement Procedures Act (“RESPA”), Regulation X, and the Truth-In-Lending Act (“TILA”), Regulation Z.

CFPB Unveils New Integrated Disclosures Under RESPA and TILA

Senate Struggles to Craft Legislation on Fannie Mae and Freddie Mac

The Obama Administration has expressed support for a bipartisan bill to wind down government-controlled mortgage companies, Fannie Mae and Freddie Mac. The proposed bill will eliminate or greatly reduce the size of these companies while retaining the federal government’s role in backing mortgage lending. However, lawmakers seem unlikely to produce a bill by the end of the year as planned.

Consumer Financial Protection Bureau Clarifies New Mortgage Servicing Rules

The Consumer Financial Protection Bureau (CFPB) recently issued an interim final rule, as well as an explanatory bulletin, to further detail and clarify the requirements of the agency’s mortgage servicing rules that were finalized in January 2013 (the Servicing Rules). The Servicing Rules implement the provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) amending the Real Estate Settlement Procedure Act of 1974 (RESPA) and the Truth in Lending Act (TILA) to provide borrowers with more detailed information regarding their loans, ensure that borrowers are not unexpectedly assessed charges or fees, and inform borrowers of alternatives to foreclosures.

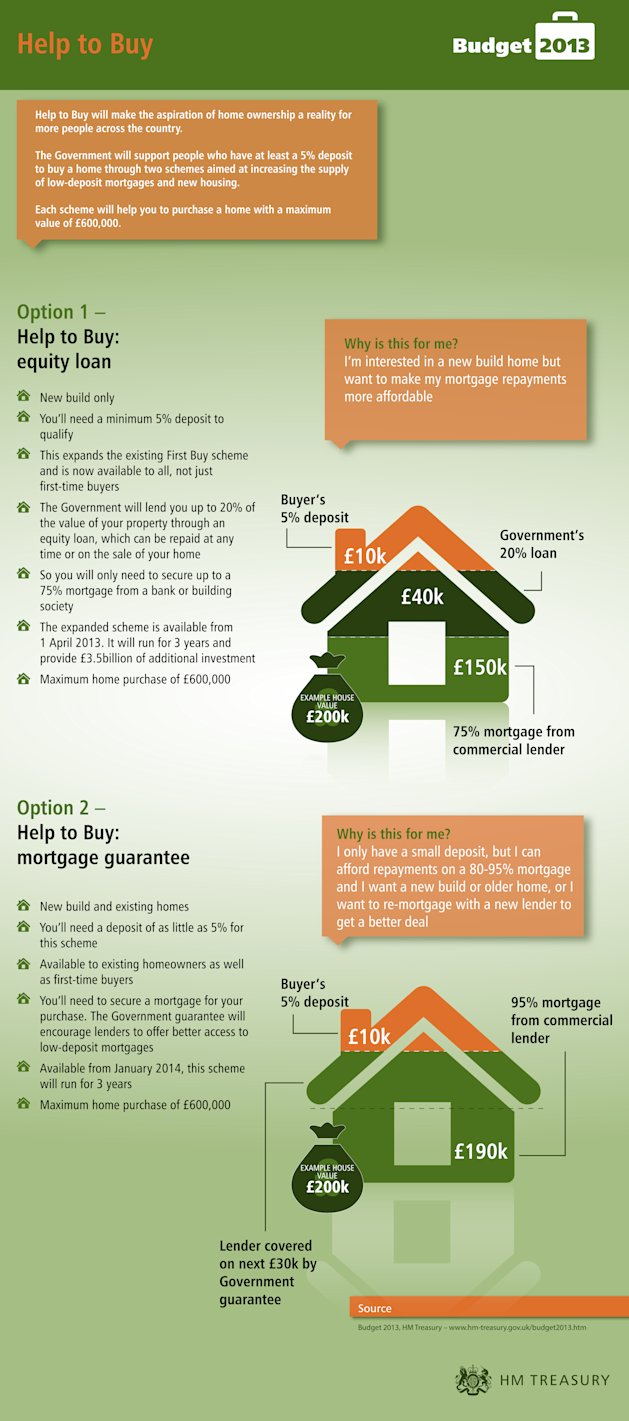

Controversial Second Phase of Help to Buy Plan Now Underway

Last Tuesday, October 8, 2016, England enacted the second phase of its Help to Buy plan, which encourages low-deposit borrowing for purchases of newly built and already existing homes. The first phase of the plan was enacted this April, and the plan is set to run for the next three years.

Under the first phase, the government will provide a 20% equity loan toward the purchase of a new home priced at £600,000 or less when the purchaser deposits 5% of the purchase price up front. These loans are interest free for the first five years, accrue at an interest rate of 1.75% for the sixth year, and accrue at a floating rate of 1% plus the Retail Price Index inflation rate for every subsequent year.

{kind=link}

Under the second phase, registered lenders, who have paid the necessary fees to the government, may offer a mortgage covering up to 95% of the purchase price of a new or existing home valued at £600,000. The purchaser, however, is required to deposit 5% of the value up front. In return, lenders will receive a seven-year guarantee from the government covering 15% of the loan value.

The four participating lenders have already revealed their rates, but some lenders have been more reluctant to join the program. RBS and NatWest are offering a two-year, no fee fixed-rate mortgage (FRM) starting at 4.99% for those depositing 5% of the home value. Halifax is offering a starting rate of 5.19% with a £995 fee. While somewhat competitive for the low-deposit market, these rates are not competitive with higher-deposit rates.

Privy Council Rules on the Court’s Equitable Jurisdiction to Set the Financial Terms of Relief against Appropriation

[Editor’s Note: The following post is authored by Ropes & Gray LLP]

Last week the Board of the Privy Council delivered a critical sequel to its previous judgments in connection with the Cukurova Group’s attempt to recover shares following an appropriation. The Board held that not only can the court reopen an appropriation and exercise its jurisdiction to grant relief from forfeiture after the event, as per its decision earlier this year, but it can also exercise its jurisdiction to determine the basis and conditions of such relief.

For mortgagors and borrowers in secured transactions, the decision provides a helpful guide as to the breadth and flexibility of equity’s ability, after forfeiture, to intervene in their favour and adjust the contractual terms where it would be unconscionable to enforce them strictly. (more…)

FTC Wins Injunction Against Defendants Promising Mortgage Relief

Recently the FTC won injunctive relief after filing a complaint against ten phony mortgage relief operations. The complaint alleges that three individuals and seven companies “prey on financially distressed homeowners by luring them into membership programs or loan modification services with promises that they will receive legal representation . . . to save their homes from foreclosure.” Defendants charged up-front fees and then failed to follow through on their promise of services. A temporary restraining order was issued against Defendants, freezing their assets and shutting down their businesses and websites. (more…)

CFPB Finalizes Rule on Mortgage Loan Originator Compensation and Qualifications

[Editor’s Note: The following post is authored by Arnold & Porter LLP]

I. BACKGROUND

On January 20, 2013, the Consumer Financial Protection Bureau (CFPB) issued its final rule (the Final Rule) regarding mortgage loan originator compensation and qualification requirements1 under the Truth in Lending Act (TILA), as amended by the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Dodd-Frank Act). The Final Rule modifies existing compensation and qualification requirements under Regulation Z. It prohibits a creditor from compensating a loan originator based on a term of a transaction or a “proxy” for a term of a transaction. It also codifies the existing ban on “dual compensation,” in which a loan originator receives compensation from the consumer and an additional party other than the originator’s organization, but creates an exception allowing a loan originator organization to pay its employees or contractors a commission provided that the commission is not based on a term of a loan. The Final Rule provides a complete exemption from the statutory ban on the consumer payment of upfront points and fees. The Final Rule also includes requirements regarding loan originator qualifications, licensing, and recordkeeping, and implements statutory provisions regarding mandatory dispute resolution and the financing of credit insurance in connection with a residential mortgage loan. (more…)

Weekly News Update: Bank Violations and Protecting Confidential Information

Last year the $25 billion National Mortgage Settlement meant to end mortgage servicing abuses was announced by federal and state officials; however, there is mounting evidence that not all the involved banks are living up to their commitment. The five banks involved with the settlement are Bank of America, Wells Fargo, JPMorgan Chase, Citigroup, and Ally Financial Inc. In a recent letter, New York Attorney General Eric Schneiderman claims that Bank of America and Wells Fargo are violating the terms of the settlement. Schneiderman states that the two banks have committed a combined 339 violations of servicing standards, including deliberate delays by Wells Fargo and Bank of America to reviewing loan modification applications, a practice reminiscent of the “same misconduct that precipitated the National Mortgage Settlement.” Schneiderman has plans to sue both banks for failing to uphold their obligations under the settlement. However, in a letter to Schneiderman, Bank of America responded that they cannot be sued since they have not been given ample time to remedy their alleged violations. Both Bank of America and Wells Fargo say they remain committed to the terms of the settlement and deny that they have committed violations.

According to a recent story published by Corporate Crime Reporter, the proxy advisory services firm Institutional Shareholder Services (ISS) was fined by the SEC for failing to prevent one of its employees from distributing confidential material. In exchange for information revealing how more than 100 ISS institutional shareholder advisory clients were voting their proxy ballots, the employee, who no longer works at ISS, received expensive tickets to concerts and sporting events, meals, and an airline ticket. The SEC investigation revealed that ISS lacked sufficient controls over access to confidential client vote information, allowing for the employee to gather the data. As a result of the failure of ISS to protect its confidential information, the SEC has required ISS to pay a $300,000 penalty and allow for an independent compliance consultant to review its procedures and ensure they comply with the Investment Advisers Act’s requirements for treatment of confidential information.

HUD’s New Fair Housing Rule Could Face Supreme Court Scrutiny

The Housing and Urban Development Agency (HUD) recently issued a new “disparate impact” rule – essentially codifying the main method used to prove housing and lending discrimination for the past several decades – but the timing of this move may say more than the rule itself. The new rule has come into effect while the Supreme Court is deciding whether or not to hear a critical housing discrimination case, Mount Holly v. Mt. Holly Gardens Citizens in Action. If the Court grants cert, it has the potential to overturn the very substance of HUD’s new rule and, more importantly, the “disparate impact” method of fighting housing and lending discrimination in general. Among the many stakeholders, this has considerable impact on the banking and insurance industries, which have faced an increase in lending and rate-setting discrimination lawsuits based on “disparate impact” claims. You can read the HUD rule here, and you can read the Mount Holly petition for a writ of certiorari here.

In the case, the Mount Holly Township in New Jersey determined that a residential area known as “the Gardens” was blighted, and it moved forward with redevelopment plans for the area. Although the Township acquired and demolished most of the houses in the area over several years, it failed to build new housing. Residents of “the Gardens” eventually sued and won on the claim that the Township’s actions have had a disparate impact on African Americans. On appeal before the Supreme Court, the Township now raises the question whether “disparate impact” is a cognizable claim for proving discrimination under the Fair Housing Act.

As the agency responsible for enforcing the Fair Housing Act, HUD works to sniff out illegally discriminatory housing practices based on protected characteristics (e.g., race, ethnicity, disability, etc.). It has long interpreted the Act so that even where discriminatory motivation is missing or hard to prove, HUD can still prosecute lenders or landlords, for example, if their practices cause protected persons to suffer unjustified and disproportionate harm. This is known as the “disparate impact” principle that is now codified into the rule. Based on a three-part burden-shifting test, the rule often makes it easier for plaintiffs to establish a practice as discriminatory since they do not have to prove the more subjective motivation behind that practice.

HUD’s reason for promulgating the rule is simple enough on its face: the agency wants to ensure a formalized, consistent application of the “disparate impact” principle nationwide. At the same time, HUD and the Obama administration are also likely taking proactive measures in light of Mount Holly, given that the principle may have a better chance of surviving the Court’s review if backed by a codified federal regulation.

More broadly, this decision could have significant implications for home insurers and banking institutions like Wells Fargo and Bank of America, which have been the latest targets of discriminatory lending lawsuits. The Obama administration has relied heavily on the “disparate impact” principle to go after discriminatory mortgage lending practices, pointing to data showing higher interest rates and less favorable loan conditions provided to minority persons. In the process, the administration has won some of the largest settlements in history worth hundreds of millions of dollars for minority communities across the country. Banks maintain that these settlements are the undue cost of avoiding litigation rather than any real finding of discrimination, and that the inevitable result is a transferred cost to the consumer. The American Banking Association, in particular, has expressed concern that HUD’s rule creates “unnecessary compliance risk,” which then limits credit availability and drives up the cost of borrowing in a recovering economy.

Therefore, civil rights advocates and the American Bankers Association (ABA) are well aware of the high stakes if HUD’s rule is upheld or overturned. If the Supreme Court takes the case, the waiting period begins; otherwise, HUD and civil rights advocates may have a greater sense of closure for the present.

For further reference, please see this Wall Street Journal article and this ProPublica article.

CFPB Announces “Ability to Repay” Rule for Mortgage Lenders

The Consumer Financial Protection Bureau has announced a new rule (the “Ability-to-Repay rule”) requiring mortgage lenders to ensure that potential borrowers will be able to repay their mortgages. The CFPB is charged with amending Regulation Z, which carries out the Truth in Lending Act. The CFPB also implements the ability-to-repay requirements under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”). Under Dodd-Frank, creditors must make a reasonable and good faith determination that borrowers have a reasonable ability to repay the loan.

The Ability-to-Repay rule is aimed at protecting American consumers. According to the CFPB Director, the “Ability-to-Repay rule protects borrowers from the kinds of risky lending practices that resulted in so many families losing their homes.”

Under the new rule:

- 1. Lenders are required to obtain and verify financial information from potential borrowers,

- 2. Lenders must evaluate and conclude that potential borrowers have sufficient assets or income to repay the loan, and

- 3. Lenders cannot use lower, introductory “teaser” interest rates (which cause monthly payments to jump to unaffordable levels) to base their evaluation of a potential borrower’s ability to repay the loan.

In assessing whether a borrower will be able to repay their loan, lenders must generally consider the following underwriting factors: 1) current or reasonable expected income or assets, 2) current employment status, 3) the monthly payment, 4) monthly payment on any simultaneous loan, 5) the monthly payment for mortgage-related obligations, 6) current debt obligations, 7) monthly debt-to-income ratio, and 8 ) credit history.